Gabriel Holding

165

DKK

+5.1 %

Less than 1K followers

GABR

NASDAQ Copenhagen

Home Products

Consumer Goods & Services

Overview

Financials & Estimates

Investor consensus

+5.1%

+13.79%

-0.6%

-8.33%

-34.52%

-38.43%

-72.27%

-73.6%

-13.16%

With roots back to 1851, Gabriel is today a niche company within the global furniture industry, which throughout the value chain, from idea to furniture user, develops, manufactures and sells furniture fabrics, components, upholstered surfaces and related products and services, through its business areas Fabrics, FurnMaster, SampleMaster and Screen Solutions. Gabriel sells B2B, and is growing with the largest market participants, working closely with leading international manufacturers and major users of upholstered furniture, seats and upholstered surfaces.

Read moreMarket cap

311.85M DKK

Turnover

142.32K DKK

P/E (adj.) (25e)

-43.03

EV/EBIT (adj.) (25e)

211.28

P/B (25e)

1.23

EV/S (25e)

0.7

Dividend yield-% (25e)

-

Coverage

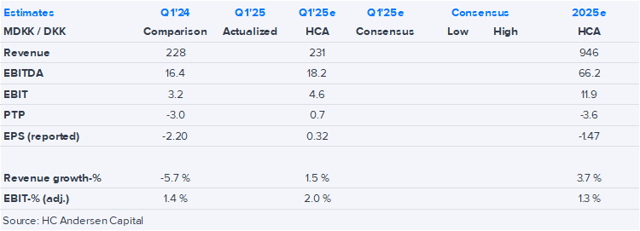

Revenue and EBIT-%

Revenue B

EBIT-% (adj.)

EPS and dividend

EPS (adj.)

Dividend %

Financial calendar

8/5

2025

Interim report Q2'25

28/8

2025

Interim report Q3'25

20/11

2025

Annual report '25

Risk

Business risk

Valuation risk

Low

High

All

Research

Press releases

ShowingAll content types

Disclosure of transactions in the shares of Gabriel Holding A/S by persons discharging managerial responsibilities and closely related parties

Gabriel Holding Q1'24-25: Q1’24-25 steady but carve-out uncertainty remains

Join Inderes community

Don't miss out - create an account and get all the possible benefits

Inderes account

Followings and notifications on followed companies

Analyst comments and recommendations

Stock comparison tool & other popular tools

Gabriel Holding Q1’24-25 preview: Carve out uncertainty raises near-term risk

Minutes of the annual general meeting on 29 January 2025

Gabriel FY'2023/24 video – Waiting for the carve-out to unlock value

Gabriel Holding FY'2023/24: Waiting for the carve-out to unlock value

Notice of annual general meeting of Gabriel Holding A/S

Irregularities in the Group’s Mexican FurnMaster company influence the 2023/24 financial year negatively and lead to corrections of previous years’ figures. Revenue for the year is DKK 912 million and the operating profit (EBIT) is DKK 10.9

Election of employee representative for the board of directors in Gabriel Holding A/S

Gabriel: FY’23/24 results delayed due to short-term uncertainties from accounts in Mexican unit

Financial reporting and general meeting for 2023/24 are postponed. Expectations for the continuing operations in the 2024/25 financial year are published.

Gabriel Holding's Chairman of the Board, Jørgen Kjær Jacobsen, does not seek re-election

Gabriel Holding A/S delivers rising revenue and operating profit (EBIT) in the third quarter of the 2023/24 financial year and maintains the upwardly adjusted expectations.

Gabriel Holding: Q3'23/24 earnings preview: Expecting seasonal softness but improving momentum

Gabriel Holding: Carve out of FurnMaster units and new growth strategy

Gabriel launches a new growth strategy to intensify development of the Gabriel Fabrics and SampleMaster business units. Carve-out of the Group’s FurnMaster units starts at the same time.

Gabriel Holding (Extensive research report video): Improving indicators suggest a return to growth